February 05, 2024

There was a noticeable dispersion in the performance between large-capitalization (cap) stocks and most other asset classes during January. The large-cap stock indices were driven higher for much of the month by better than expected news from several technology and communications stocks, such as Nvidia and Netflix. The S&P 500 index set six new record highs during the month. Other indices, including the technology stock heavy Nasdaq 100 also set new highs. However, reports showing the resiliency of the U.S. economy such as robust consumer spending, higher than expected growth in new jobs and wage increases, and improving consumer sentiment diminished the prospects for an interest rate cut by the Federal Reserve (Fed) in March. That sent prices down for interest rate sensitive assets including small and mid-cap stocks, bonds, and real estate. Most markets dropped sharply at the end of the month after chairman Powell indicated the Federal Reserve is not ready to cut rates in March and needs to see more data showing inflation is tamed. The European Central Bank head also commented that rate cut talk was “premature”. Even large-cap technology stocks erased some of their previous gains at the end of the month after Magnificent Seven companies Alphabet and Microsoft issued disappointing comments about the outlook for 2024 during their earnings reports. Oil prices rose during the month due to geopolitical issues and tighter inventories but prices for other commodities including industrial metals declined reflecting the continuing weakness in demand particularly from China.

Market Indices – January 2024

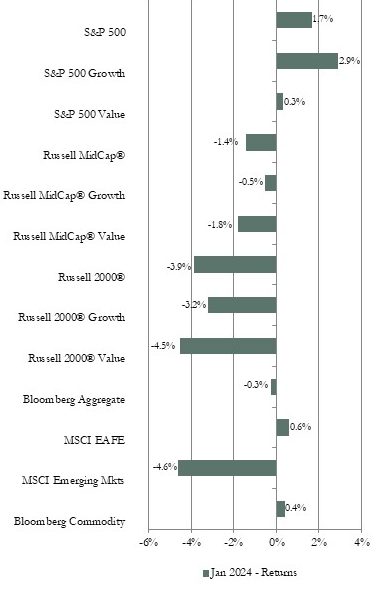

As noted above, major U.S. equity market index returns were mixed for the month. The S&P 500 index, with a positive return, outperformed the Russell Midcap index and the Russell 2000 index which both had a negative return. Growth outperformed value in all three indices. Strong returns by information technology and communications services companies drove the S&P 500’s gain due to some better than expected earnings reports and optimism about artificial intelligence related products. Communications was the top performing sector in the Russell Midcap and information technology was the performance leader in the Russell 2000. Interest rate sensitive sectors, such as utilities and real estate, were among the weakest performing sectors in each of the three

As noted above, major U.S. equity market index returns were mixed for the month. The S&P 500 index, with a positive return, outperformed the Russell Midcap index and the Russell 2000 index which both had a negative return. Growth outperformed value in all three indices. Strong returns by information technology and communications services companies drove the S&P 500’s gain due to some better than expected earnings reports and optimism about artificial intelligence related products. Communications was the top performing sector in the Russell Midcap and information technology was the performance leader in the Russell 2000. Interest rate sensitive sectors, such as utilities and real estate, were among the weakest performing sectors in each of the three

market capitalization categories as bond yields rose in reaction to stronger than expected economic data and an uptick in inflation rates that reduced the likelihood of an interest rate cut in March.

The MSCI EAFE index of developed international equities posted a small positive return but the MSCI Emerging Markets index (EM) had a sizeable negative return on a U.S. dollar basis. Since the value of the U.S. dollar rose during the month, local currency based returns were higher than dollar based returns for both indices. Growth stocks outperformed value stocks in the EAFE but value outperformed growth in the EM. Information technology and consumer discretionary were the top performing sectors in the EAFE index while energy was the top performer in the EM index. Materials was the laggard among the 11 sectors in the EAFE index while consumer discretionary was at the bottom of the performance rankings in the EM index. On a geographical basis, among developed international markets, the Far East index outperformed the Europe and Pacific ex-Japan indices. In emerging markets, Egypt, Turkey, and India had the top returns. China and Chile were the weakest performing. A main index of mainland China stocks hit a five-year low during the month reflecting the impact of the continuing weakness in consumer and business sentiment related to the property sector issues.

U.S. bond market sector returns were mixed for January. Short and intermediate maturity bond indices posted small positive returns while longer-term bond indices had negative returns since yields rose during much of the month. Yields moved up in large part because consumer price reports and certain economic data came in higher than expected which cooled optimism for a rate cut by the Fed in March. That strong economic data helped corporate bonds outperform government bonds. The Treasury bond yield curve remains inverted. The 3-month Treasury bill yield was 5.4% compared to the 2-year Treasury bond yield of 4.3% and the 10-year Treasury bond yield of 4.0%.

The Bloomberg Commodity index had a small positive return of less than 1% for January. Sub-index returns were mixed. The petroleum and livestock sub-indices had the largest gains in the high single-digit range. The price of oil moved up as geopolitical tensions in the Red Sea corridor continued to impact shipping routes and reports showed tight inventories in the U.S. The price of West Texas Intermediate crude moved up to over $77 per barrel from $71.89 at year-end 2023. Lower cattle herd numbers continue to push livestock prices up. The grains, precious metals, and industrial metals sub-indices each had a negative return.

Vogel Consulting, LLC (Vogel) Tactical Recommendations

Even though the rate of inflation has come down significantly from peak levels, inflation is likely to continue to be a main focus for investors. The resilient labor market is still an inflationary force which could make inflation more sticky than many investors seem to currently expect. Sticky inflation could mean high for longer interest rates that could pressure consumer and business spending. Therefore, markets may experience large swings in reaction to clues to the path of interest rates in economic data reports and comments by company executives in earnings reports.

Our neutral view on growth relative to value remains in place as we prefer to have exposure to sectors benefiting from longer-term secular growth trends along with some exposure to cyclicality. We retain our neutral weight position recommendation for U.S. equities and our underweight for emerging markets equities. We moved our recommendation for developed international equities to underweight due to expectations for slower economic growth outside the U.S. and higher inflation risks for Europe due to the disruptions in the Red Sea shipping corridor. A strong dollar could also be a headwind for foreign investment returns for U.S. investors. Since bond yields are still attractive, we encourage investors to revisit fixed income allocations. Our fixed income recommendation is for an equal weight position relative to long-term targets. We favor short to intermediate maturity bonds due to the inverted yield curve. We recommend an underweight allocation to hedge funds. We continue to recommend an overweight to cash reserves to avoid having to sell assets in a down market period to cover spending needs.

The statistical information contained in this commentary has been compiled from publicly available sources and is presented to you for your review and for discussion purposes only. The information contained in this commentary represents the opinion of the author(s) as of its date and is subject to change at any time due to market or economic conditions. These comments do not constitute a recommendation to purchase, sell or hold any security, and should not be construed as investment advice or to predict future performance. Past performance does not guarantee future results.

The statistical information contained in this commentary was derived from sources that Vogel Consulting, LLC believes are reliable, and such information has not been independently verified by Vogel. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of the Russell Investment Group. An index is not managed and is unavailable for direct investment.

Print: Download PDF:

Download PDF: