March 06, 2024

It was another record setting month in equity markets. The S&P 500 index, Nasdaq Composite index, and Dow Jones Industrial Average each set new all-time highs in February boosted by the artificial intelligence (AI) enthusiasm, good earnings reports, and increasingly optimistic views on economic growth potential. A new record was set in Japan as well. The Nikkei 225 stock average surpassed the previous high set in December 1989. Robust earnings reports, a pick-up in tourism, and yen weakness provided a boost to the Japanese equity market. Most major U.S. equity market indices posted positive returns in February for a fourth consecutive month of gains. In contrast, fixed income and commodity market returns were mixed.

U.S. economic news was mixed. The monthly payroll report was surprisingly strong. The report showed that 353,000 new jobs were added in January. This was the largest number of monthly new jobs in a year. In addition, wages grew at a 4.6% year-over-year rate, which is in excess of the 3.1% annual inflation rate as measured by the consumer price index (CPI). However, the latest CPI report came in above expectations. A key part of the report showed that the core services index increased 0.7% over the prior month, up from a 0.4% increase in December. The core goods index, however, showed prices fell 0.3% in January. The producer price index also came in higher than expected with the largest month-over-month increase in five months. Service activity continued to improve while manufacturing activity continues to be slow. The Institute of Supply Management Purchasing Managers Index for services moved up to 55.8. The manufacturing index improved modestly but remained in contraction territory at 49.1 (50 is the dividing line between expansion and contraction). The retail sales report disappointed investors with a decline of 0.8% from the prior month, which was a larger decline than forecast. The housing market continues to be weak. Existing home sales declined almost 2% from a year ago and housing starts came in below expectations down 15% from the prior month. Comments during the month from Federal Reserve Chair Powell made clear that no interest rate cut is coming in March.

U.S. economic news was mixed. The monthly payroll report was surprisingly strong. The report showed that 353,000 new jobs were added in January. This was the largest number of monthly new jobs in a year. In addition, wages grew at a 4.6% year-over-year rate, which is in excess of the 3.1% annual inflation rate as measured by the consumer price index (CPI). However, the latest CPI report came in above expectations. A key part of the report showed that the core services index increased 0.7% over the prior month, up from a 0.4% increase in December. The core goods index, however, showed prices fell 0.3% in January. The producer price index also came in higher than expected with the largest month-over-month increase in five months. Service activity continued to improve while manufacturing activity continues to be slow. The Institute of Supply Management Purchasing Managers Index for services moved up to 55.8. The manufacturing index improved modestly but remained in contraction territory at 49.1 (50 is the dividing line between expansion and contraction). The retail sales report disappointed investors with a decline of 0.8% from the prior month, which was a larger decline than forecast. The housing market continues to be weak. Existing home sales declined almost 2% from a year ago and housing starts came in below expectations down 15% from the prior month. Comments during the month from Federal Reserve Chair Powell made clear that no interest rate cut is coming in March.

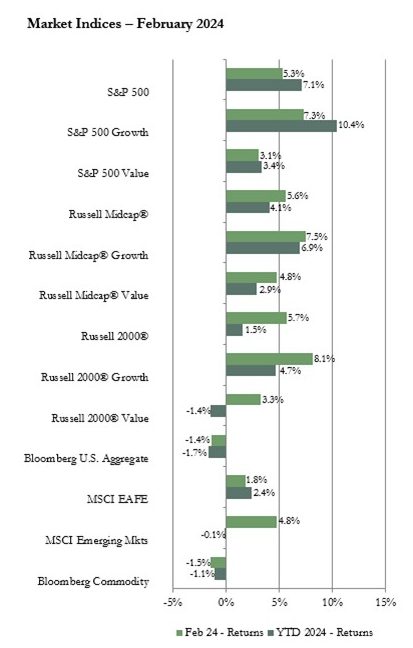

There was little difference in the monthly return for the three major market capitalization (cap) indices with the large, mid, and small-cap indices each up about 5.5%. The Russell 2000 small-cap index outperformed the Russell Midcap which outperformed the S&P 500. Growth outperformed value by a wide margin in each market cap category. Sector results varied by market cap. The top performing sector in the S&P 500 was consumer discretionary boosted by strong earnings reports from stocks such as Amazon, Lowe’s, and Home Depot. Industrials was the top performing sector in the midcap index while healthcare topped the Russell 2000 index boosted by a surge in merger and acquisition activity. As is typical in an upward trending market, the more defensive sectors, such as utilities and consumer staples, had the weakest returns.

Both the MSCI EAFE index of developed international equities and the MSCI Emerging Markets index (EM) posted a positive return for February on a U.S. dollar basis, but both lagged the returns from U.S. indices. Currency moves lowered returns for U.S. investors since local currency returns were higher than dollar based returns for the EAFE and EM. Growth outperformed value in both the developed international and emerging markets indices. The information technology and consumer discretionary sectors had the highest returns in both the EAFE and EM. In contrast, utilities was the laggard in the EAFE index and materials had the lowest return in the EM index. On a geographical basis, among developed international markets the Euro Area index had the highest return outperforming the Pacific ex Japan and Far East indices. Among emerging markets, China was the top performer after lagging for several months. Chinese stocks rallied in reaction to government stimulus news even though economic data in China continues to be weak. Korea and Poland were other top performing EM countries. Egypt and Mexico were the laggards among EM countries as both had a negative return.

Most sectors of the U.S. bond market posted a negative return for February as yields moved higher. The 10-year Treasury bond yield rose to as high as 4.5% early in the month after the hotter than expected CPI report and Federal Reserve Chair Powell’s comments squashed the outlook for an interest rate cut in March. The yield eased later after some weaker economic data and ended the month at 4.3% which was up from 3.9% at the end of January. In the rising yield environment, longer-term bond indices posted negative returns while shorter-term Treasury bond indices had small positive returns. Corporate bond index returns were mostly negative for the month. However, the corporate high yield index did post a modest positive return due to robust demand from income seeking investors. The municipal bond index also generated a modest positive return as strong demand coupled with limited new supply of bonds boosted prices. The average 30-year fixed mortgage rate advanced to close to 7% again as Treasury bond yields rose.

The Bloomberg Commodity index had a negative return for February. However, sub-index returns were mixed. The petroleum and livestock sub-indices had small gains. The price of oil moved up as geopolitical tensions in the Red Sea corridor continued to impact shipping routes and OPEC production cuts are expected to be expanded. The price of West Texas Intermediate crude oil moved up to finish the month at just over $78 per barrel from just under $77 at the end of January. Lower cattle herd numbers continue to push livestock prices up. The grains, precious metals, and industrial metals sub-indices each had a negative return.

Vogel Consulting, LLC (Vogel) Tactical Recommendations

The risk of recession has likely eased since the rate of inflation continues to slow, economic growth and corporate earnings have been generally solid, and increasing use of AI could power productivity improvement. However, the robust labor market and still strong wage growth keep inflation as a main focus for investors. The resilient labor market is an inflationary force so inflation could be more sticky than many investors seem to currently expect. Sticky inflation could mean high for longer interest rates that could pressure consumer and business spending. Therefore, markets may experience large swings in reaction to clues to the path of interest rates in economic data reports and comments by company executives in earnings reports.

Our neutral view on growth relative to value remains in place as we prefer to have exposure to sectors benefiting from longer-term secular growth trends along with some exposure to cyclicality. We retain our neutral weight position recommendation for U.S. equities and our underweight recommendation for international developed and emerging markets equities. Since bond yields are still attractive, we retain our equal weight recommendation for fixed income. We favor short to intermediate maturity bonds due to the inverted yield curve. We recommend an underweight allocation to hedge funds. We continue to recommend an overweight to cash reserves to avoid having to sell assets in a down market period to cover spending needs.

The statistical information contained in this commentary has been compiled from publicly available sources and is presented to you for your review and for discussion purposes only. The information contained in this commentary represents the opinion of the author(s) as of its date and is subject to change at any time due to market or economic conditions. These comments do not constitute a recommendation to purchase, sell or hold any security, and should not be construed as investment advice or to predict future performance. Past performance does not guarantee future results.

The statistical information contained in this commentary was derived from sources that Vogel Consulting, LLC believes are reliable, and such information has not been independently verified by Vogel. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of the Russell Investment Group. An index is not managed and is unavailable for direct investment.

Print: Download PDF:

Download PDF: