December 05, 2025

Again in November, artificial intelligence (AI) and Federal Reserve (Fed) interest rate decision related news were the primary drivers of finanical market movements. However, this month, the lack of economic data reports due to the longest U.S. government shutdown in history added to investor worries. The month started off with a global equity market sell-off led by profit taking in technology stocks as concerns grew about high valuations amid questions about the potential return on investment from the enourmous amount of spending on AI related software, chips, and infrasturcture. The sell-off in the U.S. accelerated after a private data company reported that year-to-date job layoffs hit a 20-year high in October and the angst surrounding the potenital negative economic impact of the government shutdown grew. The lack of  regular economic data reports due to the shutdown also fueled investor worries especially since the Fed would not have the normal data to guide interest rate decisions. The sell-off spread to the bond market with the 10-year Treasury bond yield rising to 4.16% and to the cyrptocurrency market with the price of Bitcoin plunging 20% from its record high in October.

regular economic data reports due to the shutdown also fueled investor worries especially since the Fed would not have the normal data to guide interest rate decisions. The sell-off spread to the bond market with the 10-year Treasury bond yield rising to 4.16% and to the cyrptocurrency market with the price of Bitcoin plunging 20% from its record high in October.

The rotation out of technology stocks and into healthcare and energy stocks in mid-month sent the Dow Jones Industrial Average to a new record high. However, equities turned lower again after comments from Fed officials suggested that inflation continues to be too high, which dampened forecasts for an interest rate cut at the Fed’s December meeting. Then late in the month, stocks, led by AI related, Magnificient 7, and interest rate sensitive industry names, rallied after two Fed presidents calling for a December rate cut and the release of weak economic data increased the probability of a rate cut. The S&P 500 clawed back its previous decline and ended the month just into positive territory. The 10-year Treasury yield dipped back below 4.0%.

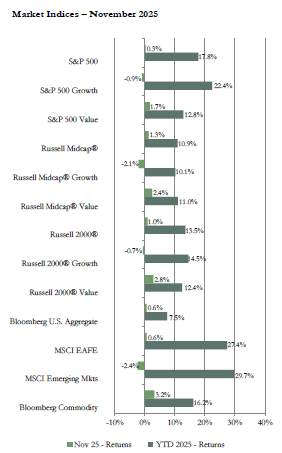

The three major U.S. equity market capitalization (cap) segment indices we track managed to post a positive return for November despite the significant volatility in the market during the month. The Russell 2000 index of small-cap stocks outperformed the large-cap S&P 500 index that was dragged down by the sell-off in the large technology and AI related companies that dominate that index. Value stocks outperformed growth stocks in each market cap category as investors favored defensive stocks and rotated into low volatility and higher dividend stocks and away from high growth momentum type stocks. Not surprisingly given the AI related sell-off, the technology sector, with a negative return, was the weakest performing of the 11 sectors in the large, mid, and small-cap indices. Healthcare was the top performing sector in the S&P 500 and Russell 2000 indices and the second best performing sector in the Russell Midcap index. The healthcare sector was boosted by positive drug development news, positive regulatory changes, and merger and acquisition (M&A) activity. Communications had the best sector return in the mid-cap index driven by M&A news.

The MSCI EAFE index of developed international equities had a modest positive return while the MSCI Emerging Markets (EM) index posted a negative return. The currency impact was a slight tailwind for the EAFE index but lowered the dollar based return from the EM index. The value index outperformed the growth index in both the EAFE and EM reflecting the weakness in AI related stocks. Information technology was the weakest performing sector in the EM and the second weakest sector in the EAFE index, behind the communications sector, hurt by worries about a bubble forming in AI related stocks. Healthcare was the top performing sector in the EAFE index boosted by pharmaceutical stocks. Materials was the performance leader in the EM index due to the strong demand for precious metals and rare earth minerals. On a geographical basis, among developed international regions, Ireland was the performance leader with the equity market there reaching a new all-time high driven by a strong economy and solid corporate fundamentals. Switzerland also had a strong return boosted by the announcement of a trade deal that will lower U.S. tariffs on imports from Switzerland to 15%. The Latin America index outperformed other emerging market regions. The leading equity index in Brazil hit a new record high on improving inflation and employment data. The technology heavy economies such as Korea and Taiwan were the performance laggards among emerging markets reflecting the global sell-off in AI related stocks.

Bond yields in the U.S. moved higher in the first part of the month as prices were hurt by the uncertainty caused by the lack of economic data due to the government shutdown and hawkish comments from Fed members. However, yields trended lower, and prices trended higher, in the second half on increasing expectations for a December Fed rate cut after soft labor market data was reported. The result was that yields ended November flat to modestly lower compared to the end of October. For example, the benchmark 10-year U.S. Treasury bond yield started the month at 4.11% but ended the month at 4.02%. November returns were positive across all sectors of the bond market and there was little dispersion between returns for the various sectors.

For the second consecutive month, the commodity index posted a return of about 3%. Most of the sub-indices we track had a positive return with livestock and petroleum the only exceptions. Livestock prices continued to decline pressured by discussions by government officials about how to lower beef prices for consumers. The petroleum sub-index moved lower as oil prices dropped due to increasing inventory levels at the same time that demand is weakening because of slowing industrial production around the world. The precious metals sub-index had the highest return due to strong price appreciation for both gold and silver. Uncertainty about macroeconomic conditions and rising expectations for a Fed rate cut drove investor demand for the metals. The price of silver hit a new record high at the end of the month.

Vogel Consulting, LLC (Vogel) Tactical Recommendations

Our outlook has not changed from last month. Capital market participants continue to navigate mixed signals. Earnings have been resilient for the most part, AI investment is providing a boost to companies in various industries and is driving expectations for increased productivity across the economy, and businesses and consumers are looking forward to the benefits of declining interest rates. In addition, it is expected that many Americans will be getting a larger tax refund in 2026 since tax cuts in the One Big Beautiful Bill were backdated to the start of 2025. The larger refunds are likely to be spent providing a boost to economic activity in the first part of next year. However, questions remain about the flow through of tariff impacts, the labor market is clearly slowing which could dampen spending and investment, and asset prices are high in many sectors particularly large-cap technology, communications, and other AI related stocks even after the temporary pull-back in November. Therefore, our view continues to be that diversification across regions and asset classes is likely to be beneficial as global economies and markets navigate potentially significant changes to policies as well as business and consumer reactions to those policies. Policy makers and investors will be closely watching data for clues to the outlook for economic activity and the impact on corporate earnings so we expect periods of volatility as markets react to cross currents in the news.

Our current recommendations are for a neutral weight position in U.S., international developed, and emerging markets equities. Our neutral view on growth relative to value remains in place as we prefer to have exposure to sectors benefiting from longer-term secular growth trends along with some exposure to cyclicality. Since bond yields are still attractive, we retain our equal weight recommendation for fixed income. We favor short to intermediate maturity bonds. We recommend an underweight allocation to hedge funds. We continue to recommend an overweight to cash reserves to avoid having to sell assets in a down market period to cover spending needs since markets are likely to be volatile in the short-term in reaction to policy, earnings, and economic news.

The statistical information contained in this commentary has been compiled from publicly available sources and is presented to you for your review and for discussion purposes only. The information contained in this commentary represents the opinion of the author(s) as of its date and is subject to change at any time due to market or economic conditions. These comments do not constitute a recommendation to purchase, sell or hold any security, and should not be construed as investment advice or to predict future performance. Past performance does not guarantee future results.

The statistical information contained in this commentary was derived from sources that Vogel Consulting, LLC believes are reliable, and such information has not been independently verified by Vogel. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of the Russell Investment Group. An index is not managed and is unavailable for direct investment.

Print: Download PDF:

Download PDF: